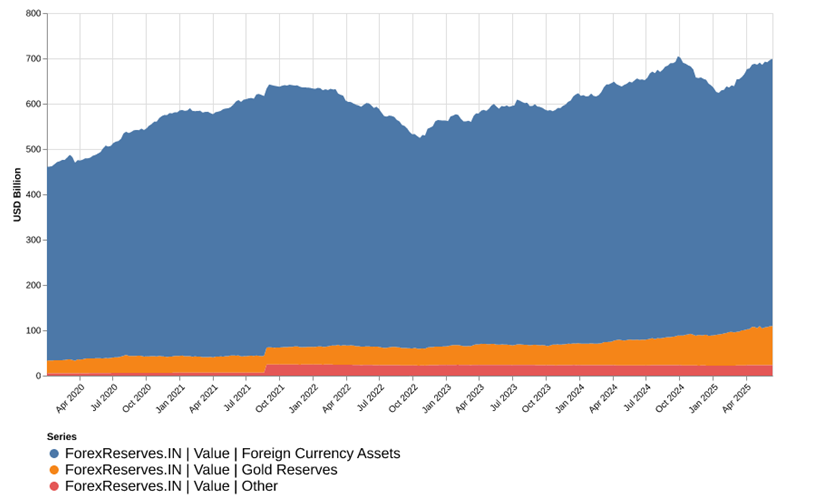

Forex reserves increase further to USD699bn, on increases in both Gold reserves and Foreign Currency Assets. This brings it close to its all time high as geopolitical uncertainities increase. The fortnightly credit growth that will be released at the end of the week should contain the earliest signal related to RB’s jumbo rate cut of 50bps in early June. As such, it will be closely monitored to see if the narrative around credit growth changes after its sharp fall to less than 9%.

Forex Reserves inch closer to USD 700 bn:

As per the latest RBI data, for the week ending 13 June 2025, India’s forex reserves increased by USD 2.3 bn week over week to USD 698.9 bn. The increase is fueled by increase in both gold reserves as well as foreign currency assets. The total value of gold reserves increased by USD 428 m to USD 86.3 bn. The total value of foreign currency assets increased by USD 1.8 bn to USD 589.4 bn. Gold reserves had increased substantially YTD. In 2025, while gold accounted for only 12% of total reserves, it contributed to 25% of incremental reserves.

Figure: Forex reserves increased sharply

Source: RBI

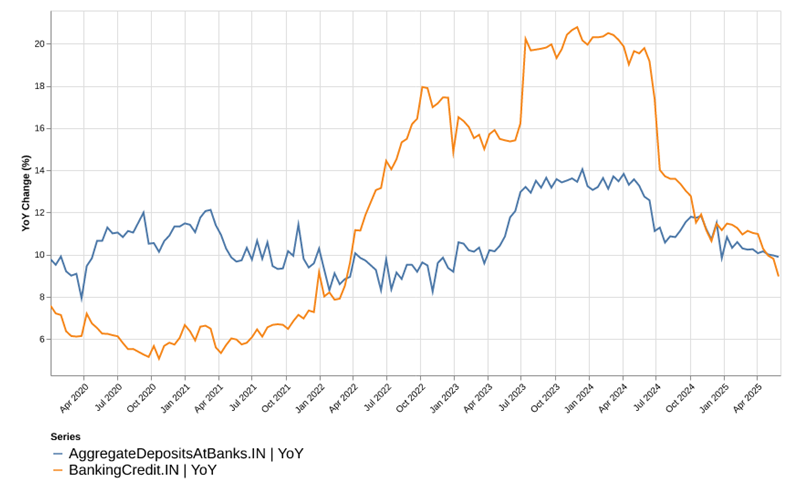

RBI’s jumbo rate cut could reflect in this week’s credit growth data:

Credit growth is under increasing focus as it had deteriorated to less than 9% as per the last release. The sub-9% growth was a first in more than 3 years. The sharp deterioration in credit growth over the past few months has even raised the question of whether the RBI rate cuts would be sufficient to improve the sentiment.

New data on credit growth will be released at the end of this week. This will be the first data on credit growth trends since RBI announced its jumbo rate cut of 50bps. As such, it will be keenly tracked for any signs of an improvement in credit growth trends.

A quick recap of India’s credit growth is that the conditions were excessively “hot” last year. During 2024, banking credit had jumped 20% on a year-on-year basis, supported by strong demand from corporates, retail borrowers as well as from services sector. The high pace was unsustainable and carried risks of asset quality deterioration and overheating in pockets of the economy.

A slowdown in both retail and corporate credit resulted in the current slowdown. A variety of factors including tighter norms for NBFC credit and unsecured retail credit (credit cards, personal loans etc) are being attributed to. While a moderation was expected, the sharp fall is increasingly a cause for worry.

Figure: Credit Growth had dipped to a 3-year low. Much slower than deposit growth

Source: RBI

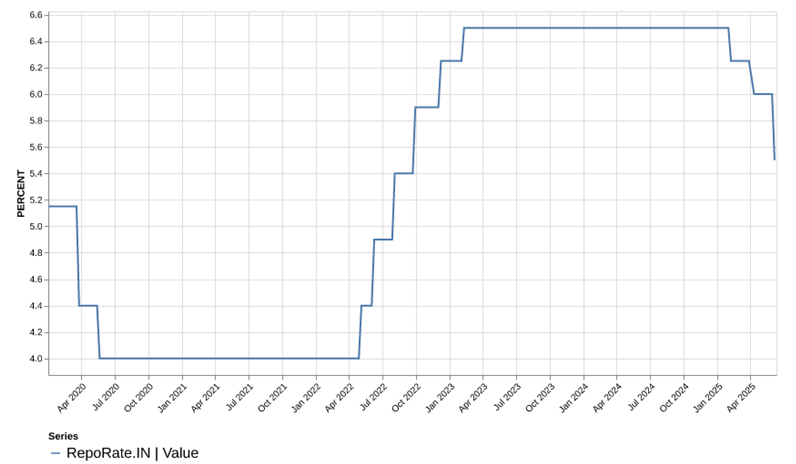

Most central banks stayed put on rate cuts:

The week witnessed a slew of central banks providing their updates on rate cuts. US, UK, Bank of Japan and People’s Bank of China had kept their policy rates unchanged. RBI had announced a jumbo rate cut of 50bps two weeks ago. This brings the total rate cuts in 2025 to 100bps. The last cut of 50bps had come as a positive surprise vs expectation of 25bps. The cut was also significant as it took the repo rate to levels not seen since 2022.

While the rate cuts had been surprising, there was also a notable change in stance in RBI’s monetary policy. It changed from ‘Accommodative’ to ‘Neutral’. In essence, this implied that further rate cuts were unlikely unless the growth surprises negatively.

Given the continued deterioration in credit growth, it remains to be seen if RBI would consider giving further impetus or adopt a wait and watch approach for the lower repo rates to reflect in lower lending rates before considering another cut.

Figure: Sharp Repo Rate cuts by RBI in 2025

Source: RBI

What is Repo Rate – A Primer

The repo rate is the rate at which the RBI lends to commercial banks. A lower rate of interest reduces the cost of borrowing for banks and can ultimately mean lower interest rates for loans to consumers and businesses. It is the primary device employed by the RBI to manage the economic activity in the country.

Goals behind a cut in the Repo Rate

Encouraging Credit Demand: By making borrowing cheaper, it encourages households, firms to borrow and spend on consumption and investment goods. That can be particularly good for rate sensitive areas like housing, auto and small business.

Boosting The Economy: Economists say Reserve Bank of India’s cut will help lift economic activity by bringing down the cost of spending and investment.

Inflation Management: The RBI’s move to reduce the repo rate comes against the backdrop of inflation moderating particularly in food prices. Retail inflation dropped, giving the central bank a room to have a more accommodative stance without actually contravening its inflation targets.

Boost Liquidity: The rate reduction is combined with steps to provide liquidity to the banking system, so banks have the required cash to lend more money.

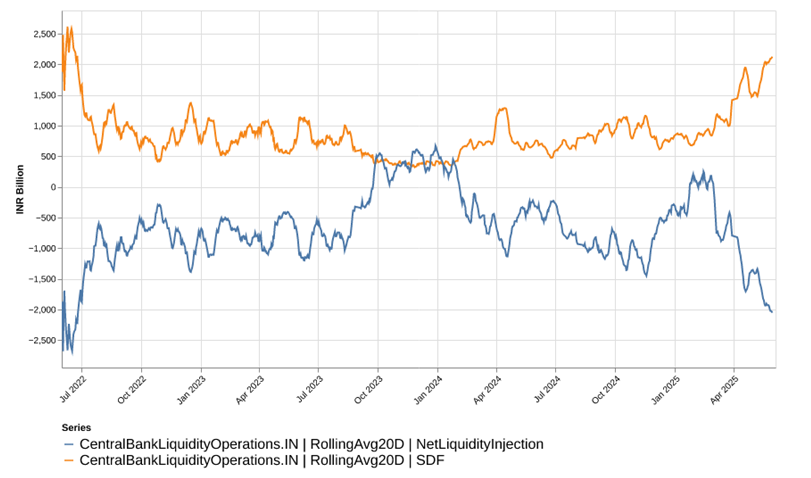

Banks continue to park their money in SDF:

One of the ways in which banks have channeled their liquidity is into SDF balances. As per RBI’s last release, SDF balances had increased to their highest level in three years. A rapid acceleration in the RBI’s daily SDF started in April 2025. Since April 2025, 20D average SDF utilization has increased significantly. The recent data shows that it has been consistently above INR 2 trn – a high not seen since 2022.

Figure: SDF utilization has spiked, absorbing liquidity

Source: RBI

What is SDF – A Primer

The SDF is a non-collateralised instrument which the banks can use for parking their surplus funds at the RBI and earn interest at a slightly lower rate than the repo. It was implemented in April 2022 as a cleaner and more efficient alternative to the conventional reverse repo.

Unlike reverse repo, the SDF does not mandate the RBI to transfer government securities as collateral, making it a more efficient tool to absorb liquidity. This has now become the de-facto floor of the RBI’s LAF corridor.

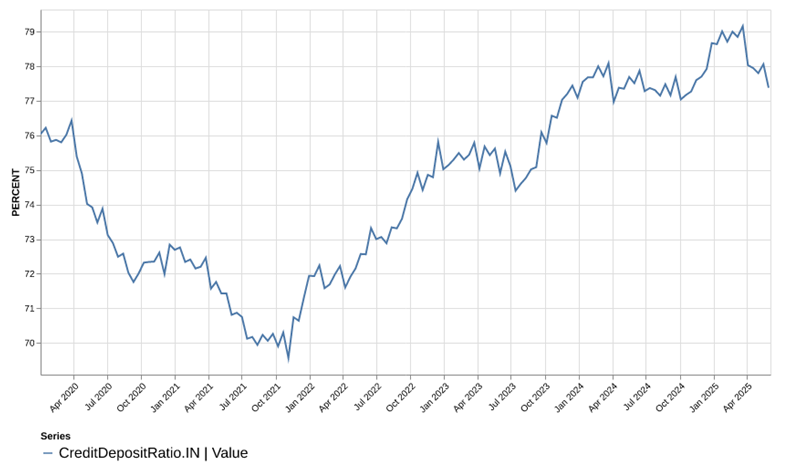

Credit Deposit Ratio – No longer a worry:

Not too long ago, credit deposit ratio was a closely watched metric as banks competed to raise deposits to meet the strong credit growth. However, the narrative on liquidity in banking has changed significantly. As credit growth slowed, banks are no longer worried about tight liquidity conditions.

As per latest RBI data, CDR has moderated from its recent peak to ~77%. A moderating CDR indicates either the relative pace of credit slowed, or deposits picked up or a combination of both happened. A closer look at the net liquidity in the system indicates that the banks parked excess funds in low interest earnings SDF facilities as the demand for credit moderated.

Figure: Credit Deposit Ratio Drops

Source: RBI

Related Tags

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, PMS SEBI Regn. No: INP000002213, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.