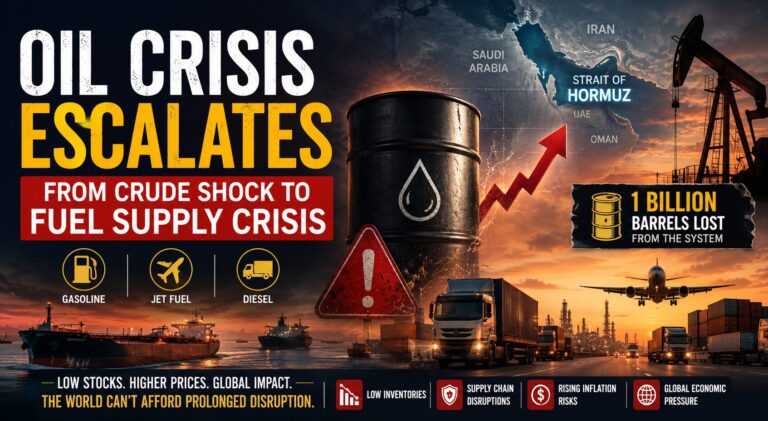

The global energy market may be entering a far more dangerous stage of the ongoing oil crisis. What began as a geopolitical shock driven by tensions around the Strait of Hormuz is now evolving into something deeper: a physical fuel supply crisis with the potential to reignite inflation, disrupt transportation systems, and pressure economies heavily dependent on imported energy.

The warning from Amin Nasser marks a critical shift in how markets are viewing the situation. According to Nasser, global stocks of gasoline and jet fuel could fall to “critically low levels” if disruptions in the Strait of Hormuz persist into the summer months.

The implications extend far beyond crude oil prices.

In the early phase of the conflict, markets focused mainly on the sharp rise in crude oil prices. Brent crude surged as traders reacted to fears of supply disruption from the Gulf region.

But the current concern is no longer merely the availability of crude oil. The bigger threat is the shortage of refined fuels such as:

This distinction is important because economies do not run directly on crude oil. Transportation systems, airlines, logistics networks, and manufacturing chains depend on refined products.

As inventories of usable fuel decline, the economic impact becomes more immediate and visible to consumers. Airline ticket prices rise, freight costs increase, and inflationary pressure spreads across supply chains.

In effect, the market is transitioning from a “crude shock” into a “fuel availability crisis.”

At the center of the crisis is the Strait of Hormuz, one of the most strategically important energy corridors in the world.

The waterway normally handles:

Even partial disruptions create cascading effects across global supply chains:

The longer tanker movement remains constrained, the more the market begins treating the event not as a temporary geopolitical flare-up but as a structural supply shock.

One of the most striking signals from Amin Nasser was his estimate that approximately 1 billion barrels have effectively been lost from the system.

The importance of this figure lies not only in its size, but in its source.

Saudi Aramco sits at the center of global crude supply chains and possesses real-time visibility into production, exports, refining, and storage flows across the Gulf.

The estimate suggests that the global market has already consumed a substantial portion of available inventories.

More importantly, replenishing these inventories may take months even after shipping normalizes.

This fundamentally changes market psychology:

The concern is no longer a temporary disruption.

It is now about a prolonged inventory rebuilding cycle.

That distinction matters because inventory rebuilding often keeps energy markets volatile long after military tensions ease.

A key point raised by Nasser is that not all stored oil is truly deployable. A significant share of reported inventories is tied up in:

As a result, official inventory figures may overstate the emergency buffer actually available to the market. This becomes dangerous during prolonged disruptions because traders and policymakers frequently assume inventories can be rapidly released to stabilize markets.

In reality, physical logistics place strict limits on how quickly stored energy can reach refiners and consumers.

The International Energy Agency and major economies are exploring coordinated reserve releases to stabilize markets. However, strategic petroleum reserves are not an unlimited solution. According to Aramco’s assessment, the combined effective release capacity of the United States and Europe may only amount to roughly 2 million barrels per day due to:

If the actual supply deficit exceeds those levels, inventories will continue declining despite reserve releases.

This is why markets remain highly sensitive to every update surrounding tanker traffic and geopolitical negotiations.

The most significant macroeconomic consequence of the fuel crisis may be the return of inflationary pressure.

Higher refined fuel prices directly affect:

These second-order effects can spread across the global economy even if crude prices stabilize. For central banks already balancing fragile growth and inflation risks, a sustained rise in fuel prices complicates policy decisions. The situation is particularly challenging for emerging economies.

For India, the risks are especially pronounced because the country imports the majority of its crude oil requirements.

A prolonged rise in oil and fuel prices could worsen:

India’s oil marketing companies could face renewed pressure if the government seeks to shield consumers from higher fuel prices.

Major state-run refiners including Indian Oil Corporation, Bharat Petroleum, and Hindustan Petroleum may experience margin stress if crude costs rise faster than retail fuel price adjustments.

The aviation sector is also vulnerable because jet fuel is among the fastest-depleting refined products globally.

Companies such as InterGlobe Aviation and Air India could face rising operating costs if jet fuel markets tighten further.

At the macroeconomic level, sustained oil inflation may also limit the flexibility of the Reserve Bank of India in managing interest rates.

Despite growing concern, financial markets are not fully pricing a permanent closure scenario. According to JPMorgan Chase, inventories could approach operational stress levels by June, increasing the probability of geopolitical de-escalation. Their logic is straightforward: The economic damage from prolonged disruption becomes increasingly costly for all parties involved. This suggests investors still expect eventual reopening of the Strait of Hormuz rather than a long-term shutdown.

However, confidence depends heavily on two developments:

Until then, volatility is likely to remain elevated.

One of the less discussed but strategically important developments is Saudi Arabia’s effort to reduce reliance on Hormuz. Saudi Aramco is expanding export flexibility through the East-West pipeline system and the Red Sea port of Yanbu. This strategy reflects a broader regional shift toward:

Over time, this could reshape Gulf energy infrastructure investment and alter global shipping patterns.

A critical insight from Amin Nasser is that reopening the Strait does not automatically restore market stability. Even after tensions ease, several problems may persist:

This means oil and fuel markets could remain volatile for months after any formal reopening. Historically, energy markets often take longer to normalize than geopolitical headlines suggest.

The current crisis can now be understood as evolving through three distinct stages.

Potential outcomes include:

Aramco’s latest warning strongly suggests the world is now transitioning from Phase 1 into Phase 2, a stage where the physical realities of energy logistics begin affecting the broader global economy.

Prices of Brent Crude are currently in the range of $105-108 per barrel, holding above $100, a critical level seen by analysts for potential domino effects on the world stock markets.

isclaimer – The story covered in this article is discussed solely for informational and educational purposes. It should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should conduct their own research or consult a financial advisor before making any investment decisions. Investments in securities market are subject to market risks. Read all the related documents carefully before investing.

Related Tags

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, PMS SEBI Regn. No: INP000002213, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.