Netweb Technologies witnessed a sharp rally of nearly 14% after CRISIL upgraded the company’s long-term credit rating from CRISIL A/Stable to CRISIL A+/Stable, while reaffirming its short-term rating at CRISIL A1. The upgrade comes alongside an enhancement of the company’s total bank loan facilities rating from ₹260 crore to ₹700 crore, reflecting growing confidence in Netweb’s financial strength, business execution, and future growth prospects.

The rating action serves as an important third-party validation of Netweb’s rapid expansion in India’s fast-growing technology infrastructure and AI ecosystem.

A credit rating upgrade from A to A+ is significant because it indicates a lower perceived credit risk and a stronger overall financial profile. Despite operating in a highly competitive and rapidly evolving technology sector, Netweb has successfully demonstrated consistent execution, healthy liquidity, and strong growth visibility.

The upgrade suggests that CRISIL views the company’s expanding scale, improving market position, and robust order pipeline as supportive of its long-term creditworthiness.

One of the key highlights behind the rating upgrade is Netweb’s remarkable revenue expansion.

The company reported revenue of approximately ₹2,183 crore in FY26, representing a revenue CAGR of nearly 70% between FY23 and FY26. Such growth rates are rare among listed technology hardware and infrastructure companies in India.

The rapid expansion highlights strong demand across enterprise computing, data center solutions, high-performance computing (HPC), and AI infrastructure deployments.

CRISIL specifically highlighted Netweb’s increasing focus on GPU-based AI infrastructure, a segment witnessing explosive demand globally.

As enterprises, research institutions, government agencies, and data centers invest heavily in artificial intelligence workloads, the need for advanced GPU servers, AI clusters, and high-performance computing systems continues to rise.

Netweb appears well-positioned to benefit from India’s growing investments in AI infrastructure, data centers, cloud computing, and digital transformation initiatives.

The company’s ability to participate in this rapidly expanding market could become a key growth catalyst over the coming years.

Another major positive is Netweb’s strong order pipeline.

The company reported:

This translates into revenue visibility exceeding ₹2,400 crore, providing confidence in the company’s growth trajectory for FY27.

A healthy order book reduces near-term business uncertainty and supports management’s ability to sustain growth momentum.

Netweb maintains a strong financial position with:

A strong cash position not only reduces financial risk but also gives the company flexibility to invest in capacity expansion, technology development, and future growth opportunities without significantly increasing leverage.

CRISIL has indicated that Netweb’s credit profile could strengthen further if the company achieves:

Meeting these parameters could potentially support additional rating upgrades in the future.

While growth remains impressive, profitability has moderated over the past few years.

Operating margins declined from:

The decline suggests that rapid growth may be coming partly at the expense of profitability. Larger infrastructure projects often carry lower margins, while increasing competition may also be exerting pricing pressure.

Investors should closely monitor whether margins stabilize within the 13–14% range or continue trending lower.

One of the most important concerns highlighted by CRISIL is the deterioration in working capital metrics.

Gross Current Assets increased from:

Receivable days stood at approximately 112 days, while inventory days increased to around 155 days.

Higher working capital requirements can lock cash within operations and potentially increase funding needs if growth remains aggressive.

Netweb remains dependent on a relatively concentrated customer base.

The top five customers contribute approximately 65–70% of total revenue.

Such concentration creates risks including:

Diversification of the customer base will be important for sustaining long-term growth stability.

The company also relies heavily on a small group of suppliers.

Its top three suppliers account for roughly 65–70% of procurement.

Given Netweb’s dependence on imported semiconductor components and technology hardware, risks include:

These factors could impact both project execution and profitability.

Management reportedly generates approximately 30–40% of annual revenue during the fourth quarter.

This concentration can create quarterly volatility, as any execution delays near year-end may materially impact revenue and earnings performance.

The strong stock market reaction appears to be driven by multiple factors converging simultaneously:

Investors are increasingly viewing the rating upgrade as independent validation that Netweb’s rapid growth is supported by strengthening business fundamentals rather than merely short-term order wins.

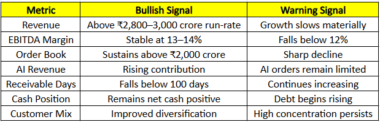

Investors should monitor the following indicators over the next few quarters:

Disclaimer – The stock/s and indices mentioned in this article is discussed solely for informational and educational purposes. It should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should conduct their own research or consult a financial advisor before making any investment decisions. Investments in securities market are subject to market risks. Read all the related documents carefully before investing.

Related Tags

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, PMS SEBI Regn. No: INP000002213, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.