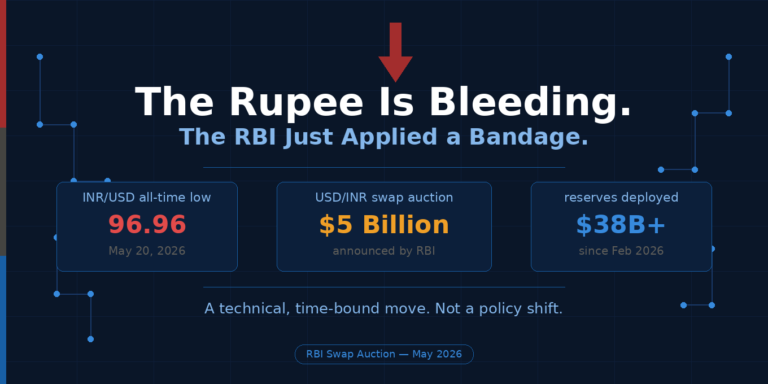

The Indian rupee is in trouble. On May 20, 2026, it hit 96.96 against the US dollar, a number that represents more than a milestone. It’s a signal. And the Reserve Bank of India read it quickly. Two days later, the RBI announced a $5 billion USD/INR buy-sell swap auction, scheduled for May 26, 2026. In this blog, we break down what that actually means, why it became necessary, and how it impacts the rest of us.

At its core, a currency swap is a temporary trade, one currency for another with a contractual promise to reverse it later. No magic. No sleight of hand. Just mechanics.

Here’s how the RBI’s version works:

Think of it as the banking system temporarily parking its dollars with the RBI and receiving rupees in return. The RBI isn’t printing money. It’s recycling what already exists using the country’s foreign exchange reserves to put liquidity back into the hands of banks that need it. Banks that lend. Banks that keep the economy moving.

Because the RBI has been fighting a currency war quietly, and expensively for months.

As the rupee kept falling; battered by rising crude prices, geopolitical tremors from the West Asia conflict, and a wave of foreign investor exits, the RBI did what central banks do: it sold dollars into the market. Flood the supply, calm the panic, slow the slide. Between February 28 and today, it has deployed over $38 billion from reserves that once peaked at $728.49 billion.

But here’s the cost nobody talks about loudly enough. Every dollar the RBI sells pulls rupees out of the banking system. That money doesn’t disappear, it just moves from banks to the RBI’s balance sheet. Do this long enough and hard enough, and you get a liquidity crunch. Banks start running short of the everyday cash they need to function, lend, and keep credit flowing.

The swap fixes that. It returns roughly ₹42,000–43,000 crore to the banking system without stoking inflation.

Three forces collided. Each was damaging on its own. Together, they were a perfect storm.

On May 21, the RBI stepped in aggressively with off-market dollar sales, triggering a sharp 70-paise intraday recovery, pulling the currency back from the brink of 97 to open at 96.30. Dramatic. Effective. But every dollar sold in that intervention drained more rupees from the system, which is precisely why the swap announced a day earlier wasn’t optional. It was essential.

No. And that distinction matters.

A swap is not a policy pivot.There’s a secondary effect worth noting. The dollars received from banks during the swap will count as reserve assets until maturity — meaning India’s reported foreign exchange reserves will show an uptick for the duration. A technical artifact of how swaps are accounted for. Not a windfall. Not a recovery. Just bookkeeping.

A weakening rupee is not just a number on a screen. It raises the cost of everything India imports, widens the trade deficit, and pushes inflation higher, at a moment when the RBI is already walking a tightrope between growth and price stability.

The swap buys time. It signals competence. The RBI is managing multiple fires simultaneously and hasn’t run out of hoses. But the underlying pressures haven’t gone away. Crude is still expensive. Geopolitical risk hasn’t evaporated. Foreign capital remains skittish.

For ordinary Indians, the impact is indirect but real. A more liquid banking system means lending rates don’t tighten unnecessarily. A more stable rupee means imported inflation doesn’t worsen. Small mercies, but mercies nonetheless.

The RBI has tools. It’s using them. What it cannot do, however, is fix the global environment that’s creating the pressure in the first place.

Related Tags

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, PMS SEBI Regn. No: INP000002213, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.