MicroFinance Institutions (MFI) started in the 1990s in India by taking inspiration from the Grameen model of Prof. Mohammad Yunus in Bangladesh. MFI industry has helped India boost financial inclusion, self-sufficiency, stability, women’s entrepreneurship, financial literacy and digitization by serving the unserved over the years. Microfinance is a type of financial service that offers loans, credit, insurance, etc. to small-scale, low-income businesses and entrepreneurs. Presently, the Microfinance industry has over 100 regulated Banks, SFBs, NBFCs, and NBFC-MFIs to serve low-income individuals in India.

MicroFinance Institutions (MFI) started in the 1990s in India by taking inspiration from the Grameen model of Prof. Mohammad Yunus in Bangladesh. MFI industry has helped India boost financial inclusion, self-sufficiency, stability, women’s entrepreneurship, financial literacy and digitization by serving the unserved over the years. Microfinance is a type of financial service that offers loans, credit, insurance, etc. to small-scale, low-income businesses and entrepreneurs. Presently, the Microfinance industry has over 100 regulated Banks, SFBs, NBFCs, and NBFC-MFIs to serve low-income individuals in India.

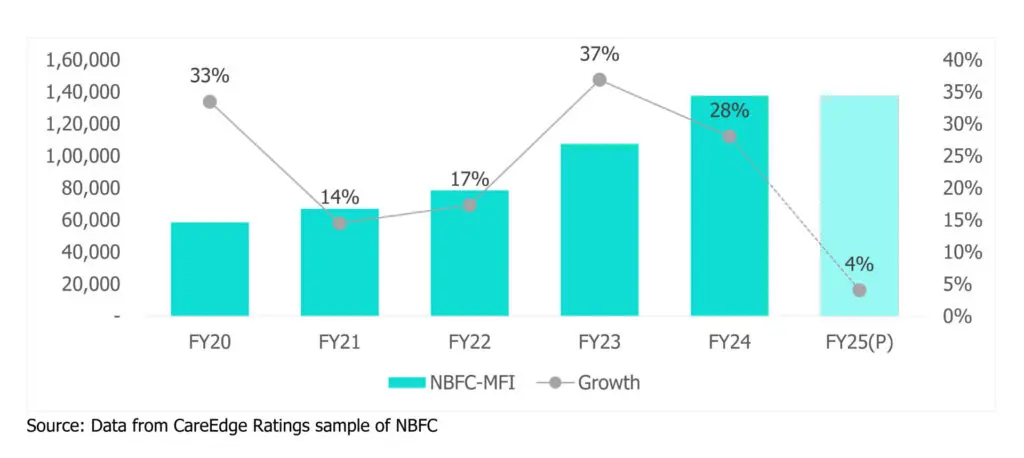

The Gross loan portfolio of the MFI industry in FY24 marked a 24.5% growth YoY to Rs. 4,33,697 crores. In Q3FY24 unsecured loans formed 9.3% of the total lending business across major banks in the country. This had inched up from 9.2% in Q2FY24. Resultant of these increases was shown in the stress books of several banks.

During FY17-24 the unsecured NBFC book grew at a CAGR of a staggering 32%. Despite the growth being off a low base it is yet double of the retail secured loans such as vehicle, gold, home and property loans during the same tenure. Another noteworthy suit of the recent shoot up in the NBFC loans is that the unsecured loans now form up 14% of the overall NBFC credit.

The growth mentioned above was partially fuelled by non-sustainable methods. Lapses in several measures across the industry have come to light. Companies pressured by steady competition across the industry were pushing growth by not adhering to the norms set out in terms of KYC or interest rates amongst others.

RBI – Timely intervention

Earmarking all the above points and the inherent risk accompanied with unsecured loans, encouraged RBI as well as MFIN to take corrective measures to curb unscrupulous methods to grow AUM by several MFI players and ensure sustainable measures are taken to avoid the formation of any sort of bubble which could hurt the financial health of the country in the future. We respect RBI’s foresight and prudence in governance and ensuring stable and strong financial health of our institutions.

Measures taken by RBI

Following the actions of the RBI, MFIN too took on corrective measures to curb the highly unsustainable growth rate. MFIN “laid down the law” by restricting incremental lending to customers:

Impact – both short term and long term

The above justified and much needed actions by the regulatory bodies resulted in a slowdown in growth and downward pressure on bottom-line was felt across the industry. In turn causing a steep correction in the stock prices of several players within the MFI space.

MFIs have scaled back their growth reducing disbursements (by 2%-40% QoQ) and shrinking loan books (by around 0.2%-12% QoQ).

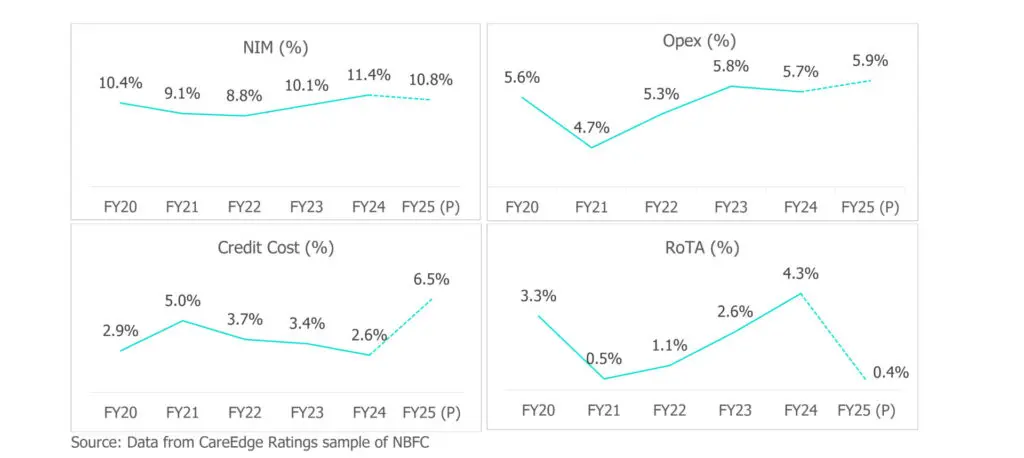

Bottom line pressure was largely felt due to deterioration of asset quality as the initiatives led to a clean-up in the books of the players. Net slippages increased by 1.3x-3.3x QoQ to 2.7%-16.1%). Accompanied with poor asset quality, weather conditions too led to a drop in collection efficiencies as well as a higher attrition (companies like Spandana Sphoorty) has in turn led to higher credit costs (increasing by 24bps-1,140bps QoQ to 2%-18.6%).

In conclusion, the changes that have been proposed and implemented by the regulatory bodies may seem extreme and even a bit harsh in the shorter term but these steps taken to solidifying the financial sector which should see a flow of benefits in the future.

These headwinds are expected to persist through the first half of FY26. It is reasonable to assume that companies with better access to capital will be in a stronger position to navigate this rough patch. We believe, companies who are able to navigate through these tough times will emerge as eventual winners in this space over the medium term. As investors, lets just wait and watch.

Ujwal Shah

Fund Manager – Equities

Related Tags

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, PMS SEBI Regn. No: INP000002213, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.