The Union Budget 2026 is one of the most important annual announcements made by the Government of India. It lays out how the country plans to earn and spend money in the coming financial year. From taxes and savings to fuel prices, infrastructure, jobs, and welfare schemes, the Union Budget influences nearly every aspect of daily life whether you’re a salaried professional, business owner, student, […]

The Union Budget 2026 stands out as a future-facing, productivity-led Budget, deeply inspired by ideas from the Viksit Bharat Young Leaders Dialogue. With a strong focus on manufacturing, MSMEs, infrastructure, healthcare, and technology, this Budget lays the foundation for long-term economic resilience amid global volatility. At its core, the Government’s Sankalp is anchored in three Kartavya, starting with accelerating economic growth by enhancing competitiveness, innovation, […]

The Union Budget 2026 is one of the most important annual announcements made by the Government of India. It lays out how the country plans to earn and spend money in the coming financial year. From taxes and savings to fuel prices, infrastructure, jobs, and welfare schemes, the Union Budget influences nearly every aspect of daily life whether you’re a salaried professional, business owner, student, […]

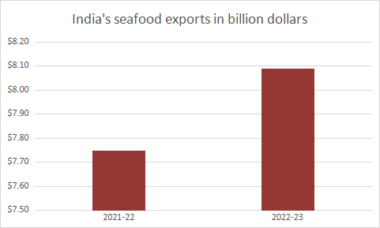

One of the few sectors for which government announced incentives in the Interim Budget is the seafood exports sector.

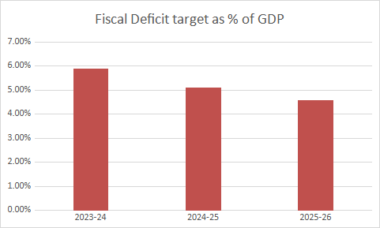

The key feature of Interim Budget 2024 is that it reiterated government’s commitment to fiscal consolidation and conservatism. It has set 5.1% fiscal deficit target for FY 25. For FY 26, the budget has projected fiscal deficit target of 4.6% of GDP. For FY 24, the revised estimate of fiscal deficit target has been kept at 5.8% of GDP. Fiscal deficit target as a % […]

Stock markets have responded blandly to the Interim Budget. At 2:25 p.m. on interim budget day, 1st February, 2024, Nifty 50 is down by 0.046%. Sensex is down by 0.086%.

Interim Budget 2024 was as per expectations. The Government did not announce any major changes. Both direct and indirect tax rates were kept unchanged; same for corporate tax rate. Revised fiscal deficit estimate for FY 24 was announced at 5.8% of GDP. For FY 25, the fiscal deficit target has been set at 5.1% of GDP. The Finance Minister once again reiterated the government’s commitment […]

Every year on the day before the Budget, the Economic Survey for the previous financial year is presented. This year the government has not presented the Economic Survey. It has probably done so because interim budget is

A demand of the oil & gas industry from the budget is to eliminate the import duty on natural gas. Currently, import of natural gas has an import duty levy of between 2.5% and 5%, depending on the form of its import. On the other hand, import of crude oil attracts 0% import duty. Elimination of import duty on natural gas will make it cheaper […]

The textile industry is a traditional industry of India. The industry has a host of expectations from the budget. It thinks that the full year budget in July will be able to meet these expectations in a better way. One expectation from the interim budget is that Remission of Duties and Taxes on Exported Products Scheme (RoDTEP) be extended till September 2024.

The real estate sector saw some slowdown in demand for affordable and middle income housing segments in the past 2 years. This happened because of successive increases in interest rates by RBI. These increases increased the cost of borrowing for home loan borrowers. The sector now expects the interim budget to provide some incentives to give a boost to demand for affordable and middle income […]

![]() IIFL Customer Care Number

IIFL Customer Care Number

(Gold/NCD/NBFC/Insurance/NPS)

1860-267-3000 / 7039-050-000

![]() IIFL Capital Services Support WhatsApp Number

IIFL Capital Services Support WhatsApp Number

+91 9892691696

Download The App Now

Follow us on

2026, IIFL Capital Services Ltd. All Rights Reserved

IIFL Capital Services Limited - Stock Broker SEBI Regn. No: INZ000164132 (Member ID - NSE: 10975 BSE: 179 MCX: 55995 NCDEX: 01249), DP SEBI Reg. No. IN-DP-185-2016, IA SEBI Regn. No: INA000000623, Merchant Banker SEBI Regn. No. INM000010940, RA SEBI Regn. No: INH000000248, BSE Enlistment Number (RA): 5016, AMFI-Registered Mutual Fund Distributor & SIF Distributor

ARN NO : 47791 (Date of initial registration – 17/02/2007; Current validity of ARN – 08/02/2027), PFRDA Reg. No. PoP 20092018, IRDAI Corporate Agent (Composite) : CA1099

This Certificate Demonstrates That IIFL As An Organization Has Defined And Put In Place Best-Practice Information Security Processes.